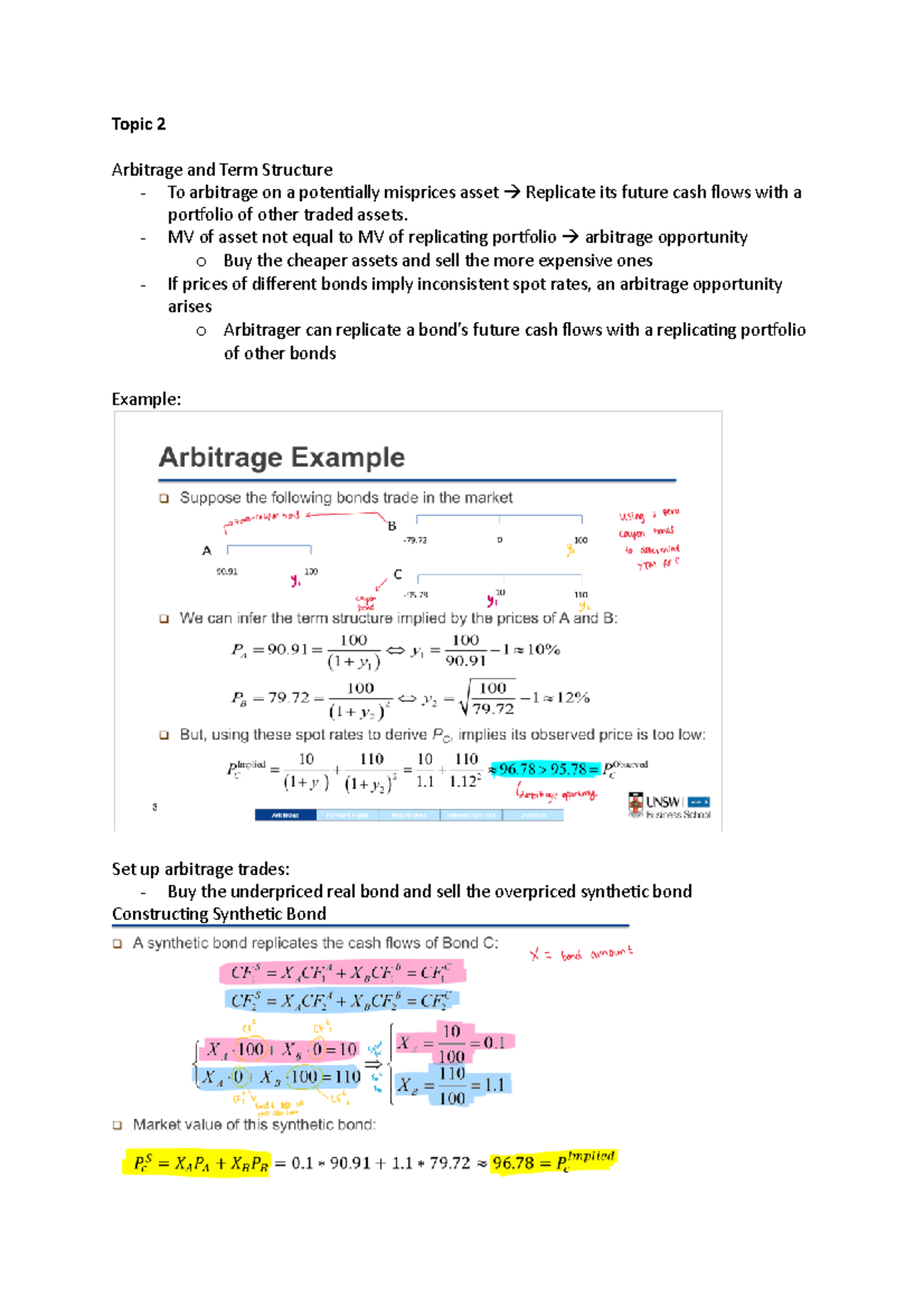

The headlines are screaming about a "wealth tax" that's finally coming for New York City’s part-time elite. On May 7, 2026, Governor Kathy Hochul and legislative leaders reached a tentative budget deal that paves the way for a recurring annual surcharge on second homes valued at $5 million or more. If you listen to the political pundits, this is the end of Manhattan’s status as a global safe deposit box.

The reality on the ground? The ultra-wealthy aren't just staying; they're doubling down.

Despite the threat of a tax that could cost a penthouse owner hundreds of thousands of dollars a year, Manhattan’s luxury market is moving at a clip that defies conventional logic. In February 2026 alone, luxury sales topped $1.38 billion. We’re seeing a surge in contracts for units priced above $20 million—the exact properties most vulnerable to this new levy. If a tax is coming to eat their lunch, why are the world’s richest people still fighting for a seat at the table?

The Math of a Safe Haven

To understand why a billionaire doesn't blink at a 1.5% or 4% surcharge, you have to stop thinking like a homeowner and start thinking like a portfolio manager. Manhattan real estate isn't just "housing" to this demographic; it’s a hedge against global instability.

While the proposed rates are steep—potentially 4% annually for properties over $25 million—they're still seen as a "cost of doing business" for capital preservation.

When you look at the 26-year performance of Manhattan condos, the average appreciation has hovered around 6% annually. Even with a new tax dragging that down, the net gain often beats holding cash in a depreciating currency or gambling in volatile foreign markets. For a buyer from China, the U.K., or Mexico, a 4% tax is a headache, but losing 20% of your net worth to a domestic currency collapse is a catastrophe. New York is where money goes to sleep soundly.

Cash is the Ultimate Shield

One of the biggest misconceptions is that these buyers are sensitive to the same pressures as the rest of us. They aren't. While the average buyer is sweating over 6.5% mortgage rates, the luxury tier has gone almost entirely "all-cash."

- 75% of Manhattan transactions in late 2025 were all-cash deals.

- Zero mortgage dependency means these buyers don't care about the Federal Reserve's next move.

- Inventory is shrinking, with listings down 21% year-over-year in early 2026.

When supply is this tight, the "buy now or lose out" mentality overrides "buy later and save on taxes." Wealthy buyers know that if they wait for the tax to be "priced in," they might lose the specific Central Park view they’ve been eyeing for a decade. In Manhattan, trophy assets are unique; they don't have substitutes.

How the Rich are Already Planning to Dodge the Bill

Don't think for a second that these owners are just going to write a check to the NYC Department of Finance without a fight. The proposal, while aggressive, is full of the kind of complexity that high-priced lawyers love.

The most obvious move? Changing residency. The tax only applies to owners whose primary residence is outside the five boroughs. For someone staring at a $250,000 annual tax bill on a $25 million apartment, the math of moving their family to New York and paying city income tax suddenly becomes a competitive option. We’re already seeing an uptick in Manhattan private school inquiries from families who previously treated their NYC pads as weekend spots.

Then there's the "rental loophole." The current draft of the tax suggests exemptions for properties that are "regularly rented out." You can expect a wave of high-end apartments to hit the "corporate suite" market, where owners "rent" the units to their own entities or third parties for just enough days to claim the exemption.

Why the Market is Ignoring the Noise

The reason the "pied-à-terre tax" hasn't crashed the market is because we’ve heard this story before. New York has been flirting with this tax since 2014. It stalled in 2019, and while the 2026 version is the closest it’s ever come to passing, the luxury market has developed a "boy who cried wolf" immunity.

Even if it passes, the effective date isn't until January 1, 2027, with the first bills not arriving until late that year. That’s an eternity in real estate. Buyers are betting that by the time the tax actually hits, the rules will have been softened, the thresholds raised, or the legal challenges will have tied the whole thing up in court for years.

The Practical Reality for Buyers Right Now

If you’re looking at the Manhattan market, don't let the tax headlines scare you into staying on the sidelines. The smart money isn't leaving; it's just becoming more tactical.

- Focus on the $4M to $4.9M range: The current proposal starts at the $5 million mark. Properties just under this threshold are seeing increased competition as buyers look for "tax-safe" luxury.

- Verify the "Primary Residence" Status: If you're buying a resale, find out how the previous owner used the unit. It will affect the property's tax history and how the city views the valuation.

- Look at Co-ops over Condos: Co-ops generally offer better value-per-square-foot and have stricter "primary residence" rules anyway, which may make them less of a target for future "absentee owner" surcharges.

The bottom line is that Manhattan is still Manhattan. A new tax might change who holds the deed, but it won't change the fact that everyone wants a piece of the skyline. If you're waiting for a "tax-induced fire sale," you're going to be waiting a very long time.

Stop watching the news and start watching the inventory. The best time to buy was yesterday; the second best time is before the spring rush of 2027 makes everyone forget this tax was even a threat.